CEO Advisory Group

CEO Advisory Group

Credit Unions Find Viable Growth Path with Bank Acquisitions

For decades, credit unions and banks experienced no crossover in their merger and acquisition strategies. Credit unions merged with other credit unions, banks acquired other banks, and neither the twain did meet.

All of that began to change about 15 years ago, when the first credit unions began exploring a new venue for growth—through the acquisition of small community banks. The appetite for such transactions has grown steadily, particularly in the last five years. Today, credit unions account for 17% of all bank acquisitions.

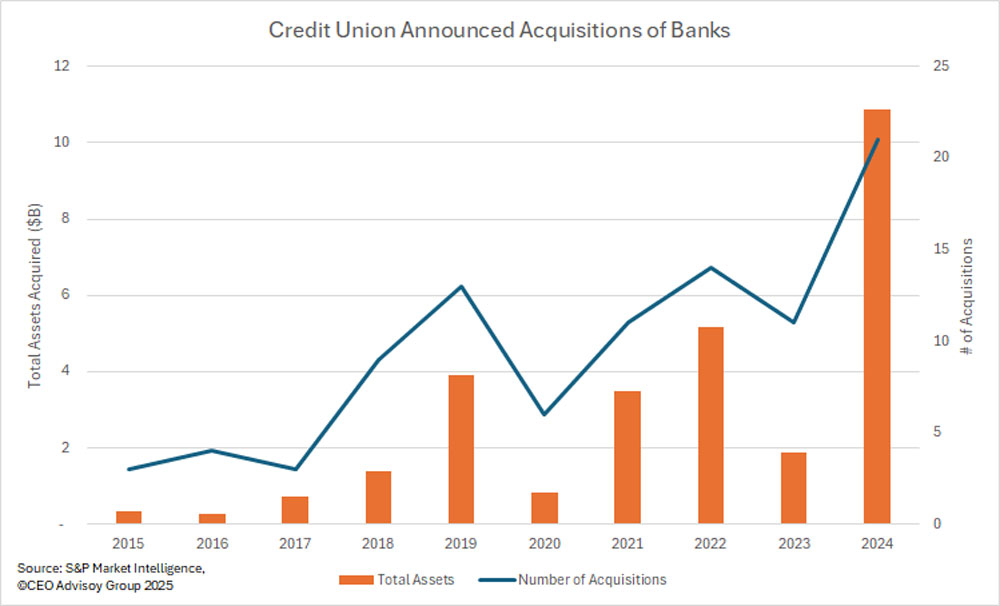

A Growing Phenomenon

Figures from the last decade show how bank acquisitions by credit unions have become more commonplace (see chart). In the five years from 2015 through 2019, there were 32 transactions equating to 6.4 deals per year. Over the last five years, 2020 through 2024, that number nearly doubled to 63, with an average of 12.6 per year.

When measuring the total bank assets acquired from those two time periods, the growth is even more remarkable. From 2015 to 2019, total assets acquired were $6.6 billion. From 2020 to 2024, that figure nearly quadrupled—to $22.3 billion.

Success Begets Success

This track record of successful bank acquisitions is having a snowball effect. Credit unions have seen the viability of bank acquisitions as a path for building asset size, membership, market share and an expanded geographic footprint. Conversely, commercial banks have found credit unions to be attractive suitors that in many cases are able to pay a better purchase price than another bank.

“A credit union-bank transaction is no longer a novelty,” says Jeff Cardone, attorney/partner with Luse Gorman, a Washington, D.C. law firm that has represented many credit unions in bank acquisitions. “Ten years ago, the bank might have said, ‘We don’t want to be blazing a new transaction trail.’ Now, there is a regulatory framework for a credit union to successfully acquire a bank, which is why these deals have become more mainstream.”

Fewer Complications

One factor that may be driving the acquisition of banks by credit unions is that they frequently find them to have fewer complications than mergers with other credit unions. A bank acquisition revolves, first and foremost, around monetary considerations, but a merger between two credit unions can sometimes get bogged down over nonmonetary factors such as how many board seats each institution will receive, what branches will remain open, or what will be the name of the surviving organization.

“We’ve seen firsthand that credit union mergers failed, despite compelling financial reasons to the deal, because the parties were not on the same page regarding key social issues,” Cardone says. “In a bank acquisition, social issues are important but clearly secondary to the purchase price. So, in many respects, a bank purchase is easier.”

As bank acquisitions become more common in the credit union sector, credit union executives need resources that help guide them in the process. Click the link to read CEO Advisory Group’s three-part whitepaper that discusses how to get started with bank acquisitions, how to proceed with a deal, and how to manage post-merger integration.