CEO Advisory Group

CEO Advisory Group

Fiduciary Duty to Consider Merger Proposal

When it comes to credit union regulations, leaders’ fiduciary duty to consider merger proposals is of the utmost importance.

Why?

Because it requires directors to act in good faith in the best interests of the membership, and in many cases, this means considering a merger with a well-positioned partner. In the past, credit union mergers were primarily driven by financial performance problems, but today, they’re an essential part of strategically positioning credit unions for the benefit of members. That means if you’re avoiding potential mergers for reasons that aren’t in the best interest of your members, you’re in breach of Section 701.4 of NCUA’s regulations.

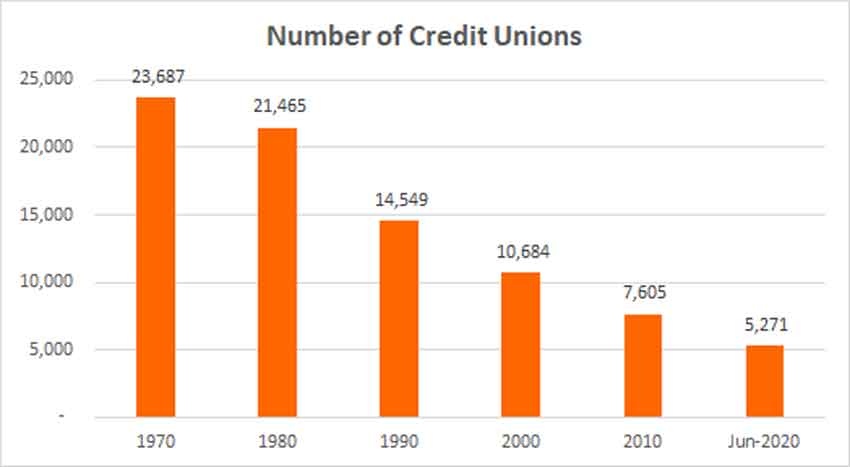

History of Credit Union Mergers

Since its peak in 1969 nearly 19,000 credit unions closed or merged . That equates to roughly one credit union per day for 51 years. For the most part, these credit unions were those with smaller assets, and generally speaking, CUs with smaller assets also have less ability to provide members with the best loan rates, products, technology, and other items that would otherwise keep them competitive.

While directors often fight against the idea of a merger, keeping the steady pace forward in an effort to stave off rebranding and the fears of the unknown that can occur when a merger is looming in the distance, as part of their fiduciary duties, leaders must put their own self-interests aside and examine solutions that are best for their members.

Credit unions with smaller asset sizes are declining while bigger credit unions are growing. From 2016 to the first quarter of 2019, the number of credit unions with more than $1 billion in assets increased from 263 to 315. That’s because directors are realizing, as part of their obligations to credit union regulations, they must consider mergers to be in compliance with their fiduciary duties.

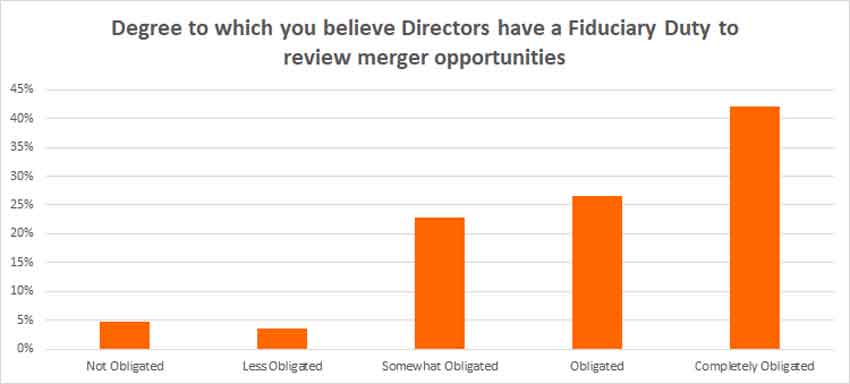

How Do Leaders View Their Roles with Regard to Fiduciary Duty?

In a survey commissioned by CEO Advisory Group, it was determined that more than 42% of credit union directors feel obligated to consider a merger proposal or inquiry. Fewer than 5% of respondents said they didn’t feel obligated to entertain such a request, while nearly half the respondents indicated they felt somewhat obligated or obligated to consider partnering with another credit union.

The overwhelming majority of respondents indicated that it’s within their fiduciary duties to consider a merger when it would be for the benefit of their employees and members. Overall, approximately one in five directors indicated that directors have a fiduciary duty to act in the best interest of the membership, and with such care, including reasonable inquiry, as a prudent person.

Your Fiduciary Duty to Consider Merger Proposal

Mergers aren’t easy, but given the current credit union regulations, consideration of such an action is incumbent upon leaders. So, when does the consideration of a merger proposal become an eminent possibility?

- Declining membership. If your credit union is struggling to grow—or even retain—members, it’s in the best interest of the organization to consider possible merger suitors who can attract and retain larger audiences. Membership bases can decline for a number of reasons, many of which also lend themselves to reasons you should consider a merger.

- Regulatory compliance. It’s a real fact that smaller organizations simply have fewer resources to deal with the seemingly day-to-day changes that occur with credit union regulations. On the contrary,

larger credit unions are able to hire people who are solely dedicated to watching and adhering to compliance requirements.

larger credit unions are able to hire people who are solely dedicated to watching and adhering to compliance requirements. - Cost structure. Marketing, technology, and branch expansion all require cash, which is something smaller credit unions may not have the luxury of having on hand. Alternatively, credit unions with large assets can maintain significant growth strategies, inclusive of the types of products and services that meet consumers’ expectations.

- Products & services. Today’s consumers have high expectations. They virtually require conveniences such as online and mobile banking, remote deposit, access to Apple Pay, and many other elements that speak to high-tech innovations. As a smaller credit union, you might not be able to provide the ever-changing elements members demand of their financial institutions. This, along with many other instances, could result in membership decline. To stay competitive, credit unions absolutely must be able to adapt to the consumers’ needs.

If you need help navigating today’s credit union regulations, reach out to a team that knows the ins and outs of the industry; download our white paper to learn more.